There was a lot of chatter about Ontario’s credit rating last week when, in a not-so-surprising move, Moody’s Corporation changed Ontario’s debt outlook from stable to negative.

Let’s be clear, this was not a downgrade in the credit rating, as some of have suggested. It’s more like the equivalent of a sad face emoticon – one way a credit rating agency has to express displeasure.

It was a statement made one day before the newly elected provincial government was set to deliver its Speech from the Throne – a speech that didn’t waiver from the promises made during the provincial election campaign that yielded this government a majority mandate.

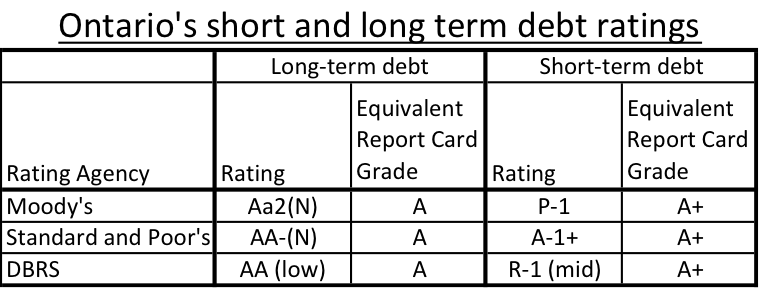

There are three main credit rating agencies that weigh in on the ability of a sovereign nation or sub-sovereign government (like states and provinces) to pay down the debt: Moody’s, Standard and Poor’s, and DBRS. Each of the three has provided very similar ratings for Ontario’s long-term debt. In fact, the change in outlook by Moody’s was an adjustment that brought it in line with S&P’s outlook.

All 3 agencies have given Ontario the second highest rating possible (for Moody’s that’s an Aa rating). It’s like receiving an A on a report card instead of an A+. The 2 and the (n) at the end of the rating are adjustments within the Aa category. A change from Aa2 to Aa3 isn’t a change in grade, but a change within the grade – like moving from and 87% on a test to an 85%.

Here are some things that the credit ratings say about Ontario’s ability to pay back its debt:

Obligations rated Aa are judged to be of high quality and are subject to very low credit risk.

—Moody’s Corporation, definition of Aa rating

Superior credit quality. The capacity for the payment of financial obligations is considered high. Credit quality differs from AAA only to a small degree. Unlikely to be significantly vulnerable to future events.

—DBRS, definition of AA rating

An obligation rated 'AA' differs from the highest-rated obligations only to a small degree. The obligor's capacity to meet its financial commitment on the obligation is very strong.

—Standard and Poor’s, definition of AA rating

And that’s just the opinion on the long-term debt obligations. On short-term debt, Ontario receives the highest possible rating from all three agencies.

Moody’s reasoned that the change in outlook was a result of questions about how this new government is going to reduce the deficit, which is estimated to be $12.5 billion – a full $1.2 billion higher than last year.

Important to point out: that deficit increase is equivalent to the decrease in the amount of revenue collected by the government as a result of a slower growing economy. This is a reality that Ontario could face for the foreseeable future.

Slower economic growth means slower revenue growth – as evidenced by the decrease in revenue when compared to the estimate last year.

Moody’s is saying that the change in outlook is the result of an increase in the deficit this year instead of another decrease. The reality is that Ontario has exceeded its deficit targets every year since the recession.

The 2014-15 budget documents indicate the province plans to exceed its 2013-14 deficit reduction target by $0.4 billion, despite the decrease in revenue.

But to reach its goal of eliminating the deficit by 2017/18 while simultaneously making some necessary investments in physical and social infrastructure, a plan will have to be deployed to get the economy revving again.

As we’ve written before – Ontario has a deficit because our economy is weak, not the other way around. And strengthening the economy must come from investment – investment we have not seen from the private sector, despite a cut in corporate income tax rates from 14% to 11.5%.

As the private sector continues to shirk its end of the bargain in Ontario, the government remains the only actor left to invest in creating jobs and rehabilitating infrastructure in this province.

Building a stronger Ontario now will bolster our ability to pay down debt in the future. More people working, means more revenue for governments and more money cycling through the economy.

A second solution to Moody’s suggestion that Ontario’s ability to pay down debt is waning: rebuild Ontario’s fiscal capacity.

The tax cutting agenda over the last 20 years has resulted in a $19 billion hole in government revenues. Between corporate tax cuts, personal income tax cuts and changes to the Employer Health Tax, Ontario’s ability to pay has been eroded to the extreme.

Rebuilding ability to pay means increasing fiscal capacity, not additional cuts to spending.

Earlier in June, Moody’s issued this announcement: Limited systemic risk and idiosyncratic features offset high debt levels of Japanese, German and Canadian sub-sovereigns. The announcement had the following to say about the credit worthiness of Canadian provinces:

Moody's says that the high debt ratings of Canadian provinces reflects their exceptional fiscal flexibility and their direct links with the local economy. Provinces display much greater fiscal flexibility than their Japanese and German peers, and have complete control over a wide range of revenue bases and full autonomy to adjust their spending from year to year.

Furthermore, Moody’s annual report on the province of Ontario had this to say:

Moody's Investors Service says in its annual report on the Province of Ontario that the Canadian province's Aa2 rating, with a stable outlook, is supported by high debt affordability and significant fiscal policy flexibility. The rating agency says that while substantial consolidated deficits and cash financing requirements are expected to continue to add to the province's stock of debt over the next several years, the province's debt burden remains manageable given its credit strengths. The rating is supported by the province's significant fiscal policy flexibility, which provides it the ability to make adjustments to both the revenue and expenditure sides of its fiscal plan in response to changing conditions. In addition, Ontario's large and diversified economy provides access to a large and productive tax base that supports the Aa2 rating.

Moody’s has been saying it for months. Last week’s announcement reiterated a message that has been delivered multiple times before:

Ontario has many options for balancing the budget while making the investments Ontario’s economy needs to get moving again – government might as well use them.

Kaylie Tiessen is an economist with the Ontario Office of the Canadian Centre for Policy Alternatives (CCPA Ontario). Follow her on Twitter @KaylieTiessen